Key Takeaways

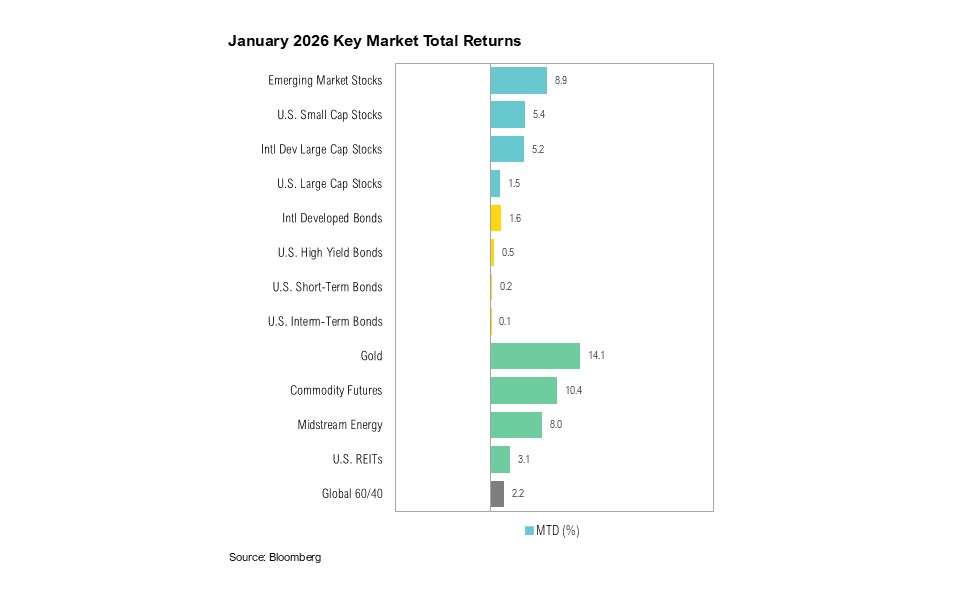

- U.S. large-cap stocks gained 1.5% in the first month of 2026 while U.S. small-cap stocks rose by 5.4%. U.S. intermediate-term bonds were flat, rising by a modest 0.1%.

- The Federal Reserve held rates at 3.50%–3.75% in January. Markets still expect the equivalent of two 0.25% rate reductions in 2026.

- Affordability, inflation, and cost-of-living concerns are top priorities for voters ahead of the midterms, driving policies aimed at housing, a proposed 10% one-year cap on credit card rates, and the “Great Healthcare Plan.”

- Mega-cap tech remains a key contributor to corporate earnings and growth, and results have been mixed.

- Kevin Warsh has been nominated as the next Fed Chair and has argued that the Federal Reserve has become a drag on U.S. economic strength, moving too slowly and relying on outdated frameworks, which he claims undermine affordability and constrain economic potential.

Overview

Markets fared well in the first month of the new year. U.S. large-cap stocks, as proxied by the S&P 500 Index, gained 1.5%, underperforming the U.S. small-cap Russell 2000 Index, which ended January up 5.4%. U.S. intermediate-term bonds, as represented by the Bloomberg U.S. Aggregate Bond Index, ended January flat, up 0.1%.

Inflation remained steady in the last month of 2025, at 2.7% year-over-year.1 Although shelter costs rose by 0.4% month-over-month (compared to 0.2% the month before), the increase was notably smaller than in recent years, which indicates a continued cooling in housing inflation.2 Progress, however, stalled in other categories. Food-at-home prices rose 0.7% month-over-month, the biggest monthly gain since August 2022.3

The U.S. economy added only 50,000 new jobs in December.4 The sectors that experienced the largest job cuts in 2025 include government (a 10% decline in the federal workforce) and professional and business services (a 1.2% decline in administrative and support staff).5 Average wages remain above inflation, rising 3.8% year over year. Consumer sentiment remained subdued in the first month of the new year, weighed down by higher prices and a weakening labor market. The Conference Board’s consumer confidence index fell from 89 to 85 in January, reaching its lowest level since May 2014 and surpassing COVID-19 lows.6 The University of Michigan’s consumer sentiment gauge ticked slightly higher, from 54 in December to 56 in January, driven by ongoing price concerns, but it remains near historic lows and 20% below January 2025 levels.7

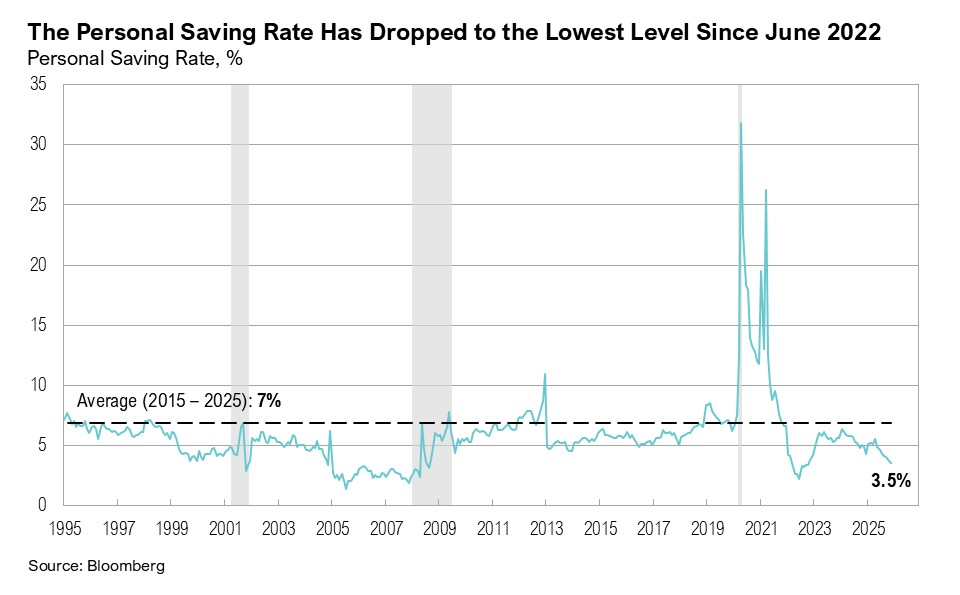

Despite muted sentiment, consumer spending has remained resilient, supported by higher-income households and a declining savings rate. The personal saving rate dropped to 2.5% in November—the most recent data available—the lowest since June 2022 and well below the 10-year average of 7%.8 According to Bank of America spending data, higher-income households increased spending by 2.4% year over year in December, while spending among lower-income households rose only 0.4%.9

As widely expected, the Federal Reserve kept interest rates unchanged at 3.50%–3.75% at the Federal Open Market Committee (FOMC) meeting on January 28. On Friday, January 30, after months of speculation, President Trump nominated Kevin Warsh as the next Federal Reserve Chair, following Powell’s term ending in May.10 His nomination had no material impact on market expectations for 2026 rate cuts, and two 0.25% reductions are still priced in for this year.11

A is for Affordability

This is a midterm election year, and recent policy proposals from the Trump administration suggest affordability is a top priority. Recent polls show that affordability, inflation, and cost-of-living concerns are the dominant election issues for voters. A December 2025 Gallup poll found that the “economy in general” was the highest-ranked economic problem. 17% of survey respondents selected it as their number one issue, followed by “high cost of living/inflation,” which 11% of respondents cited.12 A Reuters/Ipsos poll of registered voters in January showed that cost of living was the most important issue for the midterm elections, with 36% citing it as the most important issue.13 An Ipsos poll conducted in early December with over 4,000 U.S. adults found that healthcare (38%), food (21%), and housing (20%) were ranked as the most important costs for Congress to focus on.14 The January 2026 Harvard-Harris poll, conducted with registered voters at the end of January, found that “price increases/inflation/affordability” (33%) was the most important concern for voters, followed by immigration (29%) and the economy and labor market (27%).15

Trump’s approval rating, per the New York Times, is at 41% while Gallup has it at 36% (a second-term low).16 Betting market probabilities currently imply a high probability (81%) that Republicans will lose control of the House, and the odds of a Democrat sweep has ticked higher since January 24, to around 38%.17

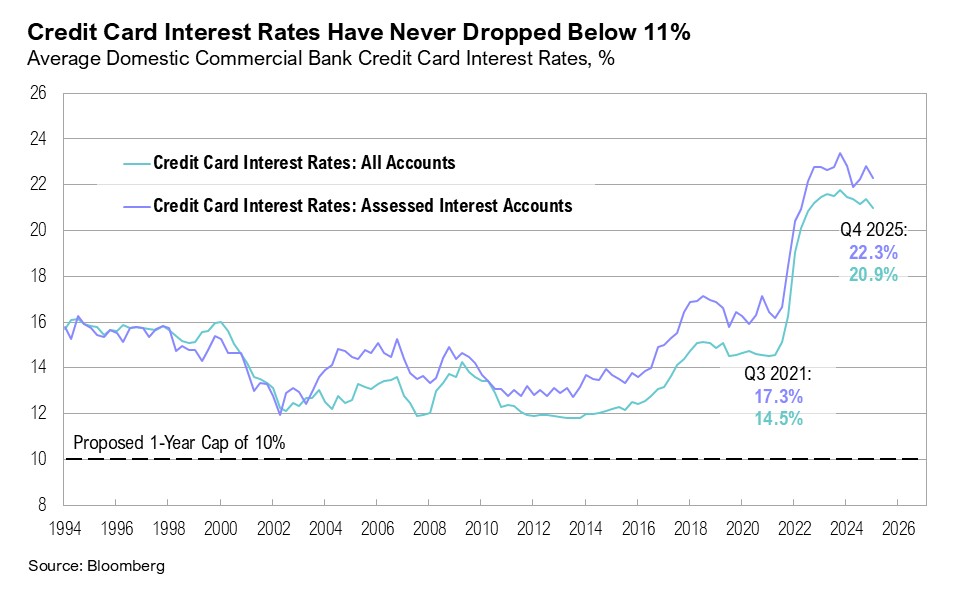

On January 9, 2026, Trump proposed a one-year 10% cap on credit card interest rates via Truth Social, demanding implementation by January 20, 2026, to protect consumers from 20-30% rates, especially subprime and lower-income borrowers trapped in debt cycles.18 This builds on campaign promises and has bipartisan legislative support, though banks warn of tighter lending and higher fees.18,19 During the fourth-quarter earnings call, Mastercard CEO Michael Miebach responded:

“It’s a really important conversation around affordability… Here is a proposal that comes with a whole range of consequences that you think through. The consequence that comes to mind first is what does this mean to credit access for a lot of the most vulnerable people that may not have access to credit any longer, should a rate cap like this be passed…”20

American Express CEO Stephen Squeri shared a similar sentiment:

“Affordability is really important. I don’t think a 10% credit card cap is the answer to that. I think it would reduce the number of cards in the marketplace. I think it would reduce line sizes. I think that it would impact small businesses and so forth, and it just has this sort of effect of a downward spiral…”21

Some banks are attempting to comply with Trump’s order via indirect measures. Both Citigroup and the Bank of America are considering introducing new credit cards with a 10% interest rate cap.22 Banking stocks did not respond well to Trump’s order. Visa, Mastercard, Wells Fargo, and JPMorgan declined 5-7% in the four trading days following the announcement. For context, national average credit card interest rates have never dropped below 11.5%.23

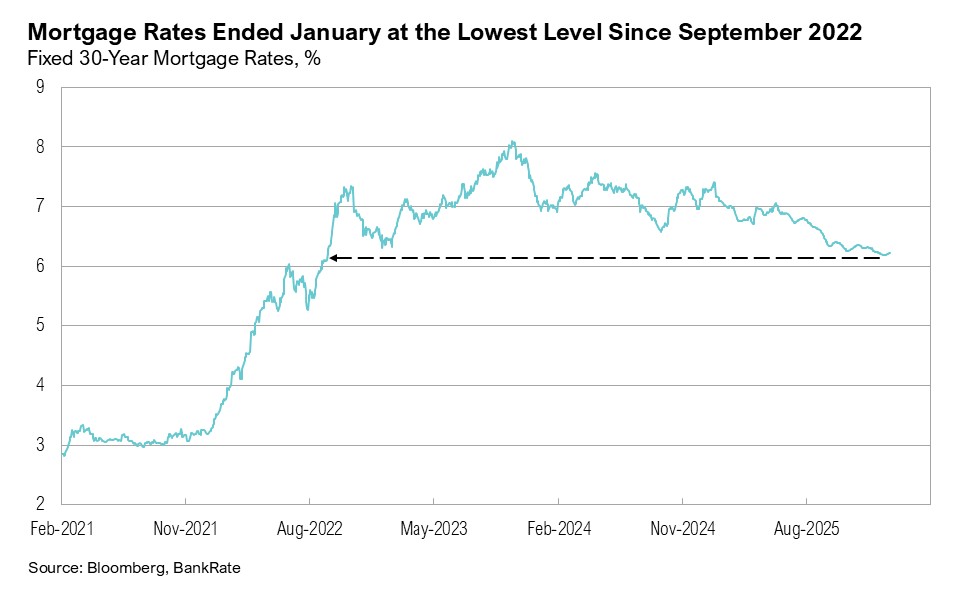

A little over a year ago, on January 22, 2025, Trump signed a presidential memorandum directing federal agencies to reduce regulatory burdens on housing construction, expand supply through innovative methods, promote efficient land use, and encourage private sector investment.24 He also issued an Executive Order on January 20, 2026, “Stopping Wall Street from Competing with Main Street Homebuyers,” banning large institutional investors from buying single-family homes and instead prioritizing individual buyers.25 Additional proposals from his January 21, 2026, Davos speech include pushing for lower mortgage rates and having Fannie Mae and Freddie Mac buy $200 billion in mortgage bonds to cut payments.26

The downtrodden real estate sector (rising just 3% in 2025, behind only consumer staples) responded well to these announcements. Mortgage rates in January reached their lowest level since September 2022, easing to 6.2%, while mortgage applications rose in tandem (29% in the second week of January and 14% in the third week).27,28 As of early February 2026, President Trump’s January 8, 2026, directive for Fannie Mae and Freddie Mac to purchase up to $200 billion in mortgage-backed securities (MBS) to lower rates is in the initial execution phase.29,30 Federal Housing Finance Agency Director Bill Pulte confirmed on January 10, 2026, that purchases have begun, leveraging Fannie Mae and Freddie Mac’s liquidity and retained portfolios, which stood at around $234-247 billion combined by late 2025, nearing their $225 billion per entity legal caps.29,30

On January 14, 2026, the government introduced the “Great Healthcare Plan,” which proposes direct-to-consumer subsidies, cost-sharing reductions for low-income families, measures to lower drug costs through most-favored-nation pricing and over-the-counter expansions, and the elimination of pharmacy benefit manager kickbacks.31 Estimates suggest these changes could lower premiums by around 10%, reduce taxpayer costs by $36 billion, and help some families avoid significant premium increases.31,32,33

Separately, the Centers for Medicare & Medicaid Services (CMS) proposed a 0.09% increase in payments to Medicare Advantage plans for 2027.34 Medicare Advantage insurers receive most of their revenue from government payments. Each year, CMS updates “benchmark” payments, which determine how much plans are paid per member. The CMS administrator said:

“These proposed payment policies are about making sure Medicare Advantage works better for the people it serves.”34

The final rates will be announced on April 6. Major U.S. healthcare providers’ share prices fell on the news. UnitedHealth led the pack with a 20% decline, following its earnings release, which warned that the company’s revenue would fall for the first time in nearly four decades.35 CVS declined by 14% on the news while Humana also declined by 20%.

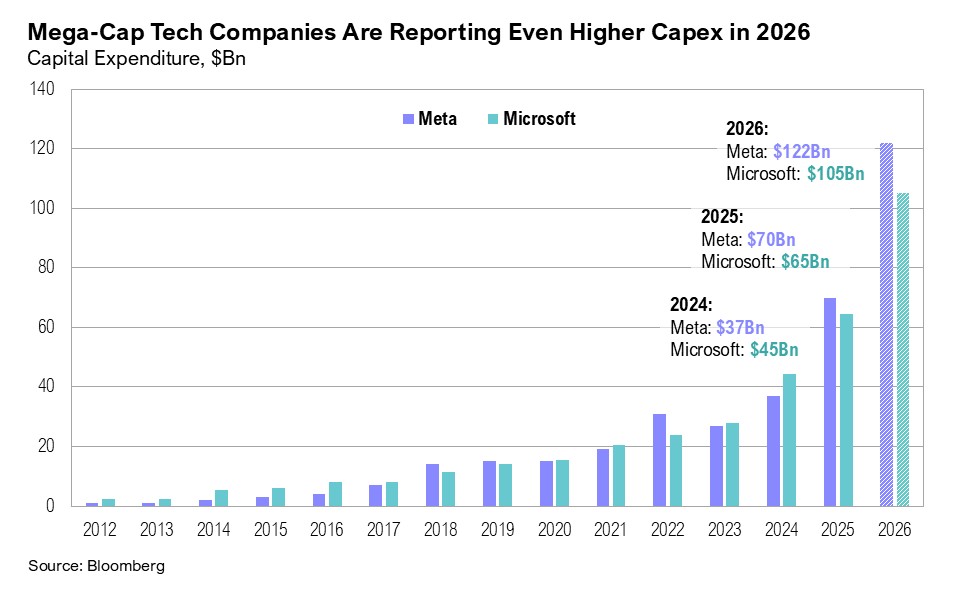

January marked the start of the fourth-quarter earnings season for 2025. By the end of the month, 33% of the S&P 500 companies had reported results. Technology (+30%) and industrials (+26%) led year-over-year growth.36 Industrials delivered surprises, contributing to upward revisions in broad earnings expectations. Most of the S&P 500’s profit margin expansion continues to be driven by technology, which represents over 30% of the index and is expected to remain a key driver through the end of 2026.36 Excluding the “Magnificent Seven,” S&P 500 earnings’ growth for the fourth quarter of 2025 is estimated at 4%; including them, growth rises to 12%.37 A similar pattern is expected in 2026, though the divergence is narrowing, suggesting a potential broadening of earnings contributions: excluding the Magnificent Seven, the S&P 493 is projected to grow 12%, rising to 14% when they are included.37 Technology (+30%) and materials (+24%) are expected to be key drivers of 2026 earnings growth.36 U.S. small-cap stocks’ earnings are expected to be stronger than their large-cap counterparts, estimated to rise 65% in 2026.38

Markets have reacted unevenly to tech earnings. Microsoft shares fell 10% following its report due to higher-than-expected spending on data centers and artificial intelligence (AI) infrastructure, a slowdown in cloud growth, and elevated capex that weighed on sentiment.39,40 In contrast, Meta shares rose about 10% despite guidance for higher 2026 capex, reflecting confidence in underlying revenue momentum.41

Concerns persist about mega-cap tech companies (particularly those at the forefront of the AI race) and their reliance on OpenAI, the creator of ChatGPT. During Microsoft’s earnings call, CFO Amy Hood noted that 45% of the company’s commercial RPO (remaining performance obligations or the value of contracted revenue not yet recognized) is tied to commitments from OpenAI.42 A Wells Fargo estimate suggests that by 2029, more than $60 billion of Oracle’s revenue (approximately 30%) will depend on OpenAI.43 Nearly all of the Magnificent Seven have entered into some form of agreement with OpenAI: Amazon is reportedly in talks to invest up to $50 billion while Microsoft and Nvidia already have active deals.44,45,46

Investors’ worries about OpenAI’s long-term revenue generation are growing. According to the Wall Street Journal, OpenAI does not aim to become profitable until 2030.47 In response to investors’ rumbling and in hopes of increasing revenue, OpenAI rolled out advertising in certain ChatGPT models across the U.S.48,49

Based on the adoption trajectories of other major technologies, like the personal computer in 1984 and the internet in 2001, AI’s adoption rate is unprecedented, reaching over 50% adoption within just three years of its release to the general public.50 By comparison, it took six years for the internet to reach a similar level and more than 15 years for the personal computer to do so.50 However, AI adoption is beginning to plateau across firms of all sizes. Roughly half of large companies now use AI in some capacity. Overall, firms that have implemented AI report only modest benefits: approximately 10% see a more than 5% improvement in decision-making speed and accuracy, while fewer than 5% report meaningful gains in time spent on high-value tasks.50 Notably, in recent earnings calls, some companies have noted that AI has significantly improved their productivity.

According to Meta CFO Susan Li:

“Since the beginning of 2025, we’ve seen a 30% increase in output per engineer… We’re seeing even stronger gains with power users of AI coding tools, whose output has increased 80% year-over-year.”51

And non-tech companies are also starting to see productivity gains. Per Bank of America’s CEO Brian Moynihan:

“We have 18,000 people on the company’s payroll who code. And we’ve—using AI techniques—we’ve taken 30% out of the coding part of the stream… That saves us about 2,000 people.”52

Markets

Emerging market stocks fared best in January, rising by 8.9%. A weak U.S. dollar, accompanied by strong performance in South America (Chile +13%, Colombia +27%) and South Africa (+8%), helped boost emerging market equities. U.S. small-cap stocks outperformed U.S. large-cap counterparts. The former gained 5.4%, and the latter ended the month up 1.5%. International developed large-cap stocks also outperformed U.S. large-cap stocks, gaining 5.2% in January. The trend was mirrored in fixed income markets: international developed bonds gained 1.6% in January while U.S. intermediate-term bonds gained only 0.1%.

Precious metals sold off sharply on the last trading day of January. Gold fell 9%, and silver plunged 26%, its largest one-day decline on record. Easing uncertainty around the incoming Fed chair lifted the U.S. dollar and triggered a broad pullback of precious metals. Despite the decline, gold ended the month up 14%.

Looking Forward

In a November 2025 Wall Street Journal opinion piece, Kevin Warsh argued that the Federal Reserve had become a drag on U.S. economic strength by moving too slowly and relying on outdated frameworks—an approach he said was hurting affordability and limiting the economy’s potential.53 He called for a pivot toward productivity-led growth driven by AI and technological advances. He argued that inflation stemmed from excessive government spending—money creation rather than wage pressures—and he urged the Fed to shrink its balance sheet while using lower interest rates to support the real economy rather than just Wall Street.53 He also advocated regulatory reform to improve credit access for smaller banks and a more distinctly U.S. approach to banking rules, rather than strict adherence to Basel standards.53 Together, these proposals framed affordability as a policy challenge that could be addressed through higher productivity, lower financing costs, and improved access to credit.

Warsh has emphasized the limits of monetary policy, favoring fiscal and regulatory reforms and balance sheet reduction over aggressive easing. More recently, he has signaled openness to rate cuts, though markets continue to view him as relatively hawkish.54 On the margin, he may prefer lower rates over balance sheet expansion as a tool for easing monetary policy, but overall, he appears to be more aligned than not with the Trump administration.

From a forward-return perspective, the starting conditions for U.S. investors are less favorable. U.S. large-cap equity valuations are elevated, credit spreads are near multi-decade lows, Wall Street’s return expectations remain broadly optimistic, and 2026 is a midterm election year, which has historically been associated with more muted returns. That said, we believe the policy backdrop supports staying the course in diversified portfolios, and we continue to see attractive opportunities in several differentiated themes—including including U.S. small-cap and international stocks along with other tactical exposures.

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

Citations

- Bureau of Labor Statistics: https://www.bls.gov/news.release/cpi.nr0.htm

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/CUSR0000SAH1

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/CUSR0000SAF11

- Bureau of Labor Statistics: https://www.bls.gov/news.release/empsit.nr0.htm

- Bureau of Labor Statistics: https://www.bls.gov/news.release/empsit.nr0.htm

- Conference Board: https://www.conference-board.org/topics/consumer-confidence/

- University of Michigan: https://www.sca.isr.umich.edu/

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/PSAVERT

- Bank of America: https://institute.bankofamerica.com/content/dam/economic-insights/consumer-checkpoint-january-2026.pdf

- CNBC: https://www.cnbc.com/2026/01/30/trump-nominates-kevin-warsh-for-federal-reserve-chair-to-succeed-jerome-powell.html

- CME FedWatch: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- Gallup: https://news.gallup.com/poll/700241/americans-end-year-gloomy-mood.aspx

- Reuters/Ipsos: https://www.reuters.com/data/which-party-do-americans-want-run-congress-2025-11-05/

- Ipsos: https://www.ipsos.com/en-us/americans-want-congress-focus-cost-healthcare-and-housing

- Harvard-Harris: https://harvardharrispoll.com/wp-content/uploads/2026/02/HHP_Jan2026_KeyResults.pdf

- Gallup: https://news.gallup.com/interactives/507569/presidential-job-approval-center.aspx

- Polymarket: https://polymarket.com/event/balance-of-power-2026-midterms

- CNBC: https://www.cnbc.com/2026/01/21/trump-congress-10percent-credit-card-interest-rate-cap.html

- BBC: https://www.bbc.com/news/articles/cp37eerlql1o

- Nasdaq: https://www.nasdaq.com/articles/mastercard-ma-q4-2025-earnings-call-transcript

- Motley Fool: https://www.fool.com/earnings/call-transcripts/2026/01/30/american-express-axp-q4-2025-earnings-call-transcript/

- Bloomberg: https://www.bloomberg.com/news/articles/2026-01-22/bank-of-america-citigroup-weigh-new-credit-cards-with-10-rate

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/TERMCBCCALLNS

- White House: https://www.whitehouse.gov/fact-sheets/2025/01/fact-sheet-president-donald-j-trump-delivers-emergency-price-relief-for-american-families-to-defeat-the-cost-of-living-crisis/

- White House: https://www.whitehouse.gov/presidential-actions/2026/01/stopping-wall-street-from-competing-with-main-street-homebuyers/

- CNBC: https://www.cnbc.com/2026/01/08/trump-mortgage-bonds-rates-fannie-freddie.html

- BankRate: https://www.bankrate.com/mortgages/30-year-mortgage-rates/

- MBA: https://www.mba.org/news-and-research/research-and-economics/single-family-research/weekly-applications-survey

- Fidelity: https://fixedincome.fidelity.com/ftgw/fi/FINewsArticle?id=202601091445RTRSNEWSCOMBINED_S0N3X7022_1

- AP News: https://apnews.com/article/pulte-mortgages-bonds-fannie-mac-freddie-mae-bd96e67f56910cbda81b7b9b3a54516c

- White House: https://www.whitehouse.gov/greathealthcare/

- CNBC: https://www.cnbc.com/2026/01/15/trump-direct-payments-health-care.html

- Wall Street Journal: https://www.wsj.com/politics/policy/trump-releases-healthcare-framework-aimed-at-lowering-costs-2716844e

- CMS: https://www.cms.gov/newsroom/press-releases/cms-proposes-2027-medicare-advantage-part-d-payment-policies-improve-payment-accuracy-sustainability

- Reuters: https://www.reuters.com/business/healthcare-pharmaceuticals/unitedhealth-forecasts-2026-profit-slightly-above-estimates-2026-01-27/

- FactSet: https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/Earnings_Insight_013026A.pdf

- FactSet: https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_012326.pdf

- LipperAlpha: https://lipperalpha.refinitiv.com/2026/01/russell-2000-earnings-dashboard-25q4-jan-29-2026/

- Reuters: https://www.reuters.com/business/retail-consumer/microsoft-edges-past-cloud-growth-expectations-2026-01-28/

- Bloomberg: https://www.bloomberg.com/news/articles/2026-01-28/microsoft-drops-after-reporting-record-spending-on-ai-hardware

- Bloomberg: https://www.bloomberg.com/news/articles/2026-01-28/meta-says-2026-spending-will-blow-past-analysts-estimates

- Microsoft: https://view.officeapps.live.com/op/view.aspx?src=https://cdn-dynmedia-1.microsoft.com/is/content/microsoftcorp/TranscriptQandAFY26q2

- TradingView: https://www.tradingview.com/news/gurufocus:085fa4ece094b:0-oracle-s-openai-ties-could-drive-60-billion-revenue/

- Wall Street Journal: https://www.wsj.com/tech/nvidia-openai-100-billion-deal-data-centers-d2f85cae

- Reuters: https://www.reuters.com/business/retail-consumer/amazon-talks-invest-up-50-billion-openai-wsj-reports-2026-01-29/

- Bloomberg: https://www.bloomberg.com/graphics/2026-ai-circular-deals/

- Wall Street Journal: https://www.wsj.com/tech/ai/openai-anthropic-profitability-e9f5bcd6

- OpenAI: https://openai.com/index/testing-ads-in-chatgpt/

- CNBC: https://www.cnbc.com/2026/01/16/open-ai-chatgpt-ads-us.html

- Apollo: https://www.apolloacademy.com/wp-content/uploads/2026/01/AIProductivityGains-012826.pdf

- Meta: https://s21.q4cdn.com/399680738/files/doc_financials/2025/q4/META-Q4-2025-Earnings-Call-Transcript.pdf

- Motley Fool: https://www.fool.com/earnings/call-transcripts/2026/01/15/bofa-bac-q4-2025-earnings-call-transcript/

- Wall Street Journal: https://www.wsj.com/opinion/the-federal-reserves-broken-leadership-43629c87

- Financial Times: https://www.ft.com/content/4ec81de7-eb59-4be8-81db-bff657e6c5d3

Index Definitions

The S&P 500 Index is widely regarded as the best single gauge of the United States equity market. It includes 500 leading companies in leading industries of the U.S. economy. The S&P 500 focuses on the large cap segment of the market and covers approximately 75% of U.S. equities.

The Bloomberg Barclays U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Duration is roughly 5 years.

The Bloomberg U.S. Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. It includes approximately 2000 of the smallest US equity securities in the Russell 3000 Index based on a combination of market capitalization and current index membership. The Russell 2000 Index represents approximately 10% of the total market capitalization of the Russell 3000 Index. Because the Russell 2000 serves as a proxy for lower quality, small cap stocks, it provides an appropriate benchmark for RMB Special Situations.

The U.S. Dollar Index is used to measure the value of the dollar against a basket of six foreign currencies: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

MSCI U.S. REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs). The index is based on the MSCI USA Investable Market Index (IMI), its parent index, which captures the large, mid and small cap segments of the USA market. With 150 constituents, it represents about 99% of the US REIT universe and securities are classified under the Equity REITs Industry (under the Real Estate Sector) according to the Global Industry Classification Standard (GICS®), have core real estate exposure (i.e., only selected Specialized REITs are eligible) and carry REIT tax status.

Disclaimers

*Source: MSCI.MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

The opinions and analyses expressed in this newsletter are based on Curi Capital, LLC’s (“Curi Capital”) research and professional experience are expressed as of the date of our mailing of this newsletter. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is it intended to speak to any future time periods. Curi Capital makes no warranty or representation, express or implied, nor does Curi Capital accept any liability, with respect to the information and data set forth herein, and Curi Capital specifically disclaims any duty to update any of the information and data contained in this newsletter. The information and data in this newsletter does not constitute legal, tax, accounting, investment or other professional advice. Returns are presented net of fees. An investment cannot be made directly in an index. The index data assumes reinvestment of all income and does not bear fees, taxes, or transaction costs. The investment strategy and types of securities held by the comparison index may be substantially different from the investment strategy and types of securities held by your account.