Summary

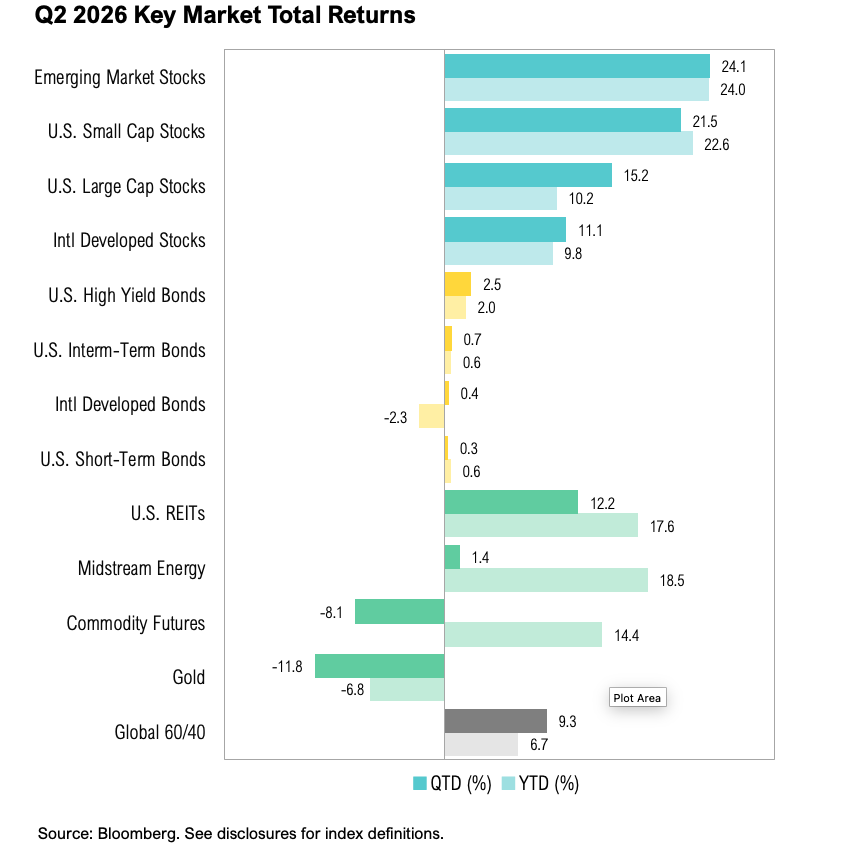

- U.S. large-cap stocks ended the quarter up 15%, and small-cap stocks gained 22%. U.S. intermediate-term bonds had modest gains, ending the quarter up 0.7%.

- The U.S. economy remained resilient as strong job growth, steady consumer spending, larger tax refunds, and improving lower-income household finances offset higher inflation.

- The U.S.–Iran conflict disrupted energy markets, pushing oil prices above $110 per barrel and gasoline prices sharply higher before conditions stabilized late in the quarter.

- The Federal Reserve entered a new era under Kevin Warsh, launching a review of its inflation framework, communications strategy, balance sheet policy, and the role of AI-driven productivity.

- AI remains a dominant market theme, but investor focus shifted from AI spending to AI returns, contributing to broader market leadership beyond mega-cap technology.

Overview

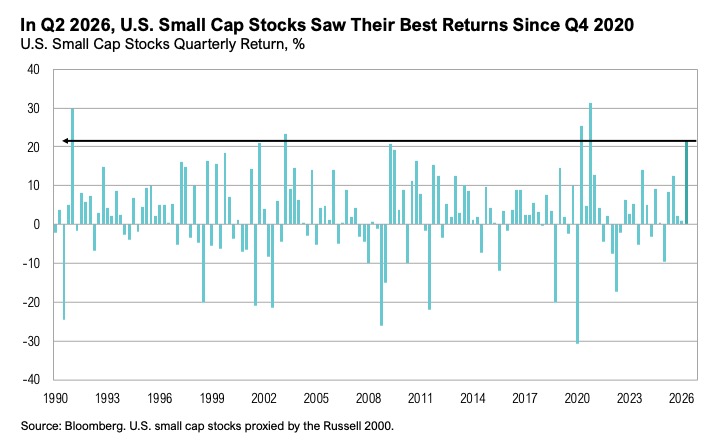

The whistle has blown on a quarter defined by geopolitical tensions and a continued artificial intelligence-related investment boom, set against the backdrop of a domestically hosted FIFA World Cup and the 250th anniversary of U.S. independence. U.S. large-cap stocks, as measured by the S&P 500 Index, closed at a new all-time high on June 2 and finished the quarter up 15%. U.S. small-cap stocks, represented by the Russell 2000 Index, performed even better, gaining a noteworthy 22%—their strongest quarterly return since the fourth quarter of 2020, when the index advanced 31%. U.S. intermediate-term bonds, as measured by the Bloomberg U.S. Aggregate Bond Index, posted a modest gain of 0.7%.

The labor market remained resilient throughout the second quarter. The U.S. economy added 365,000 new jobs over the past three-month period, despite continued layoffs in parts of the economy.1 The technology sector remained the center of job cuts in the first half of 2026.2 For the fourth consecutive month, artificial intelligence was cited as the primary driver of layoffs, with 23% of all announced job cuts in the first half of the year attributed directly to AI.2

The U.S. consumer also remained surprisingly strong. Personal spending increased by 0.4% in April and 0.7% in May.3 Meanwhile, wage growth (3.5% year-over-year in June) has not kept pace with inflation (4.2% year-over-year in May, the most recent reading).4 Larger-than-usual tax refunds following the passage of the One Big Beautiful Bill in July 2025 appear to have supported spending. Tax refunds were 18% higher than a year earlier, and the average refund increased about 12% to $3,280.5

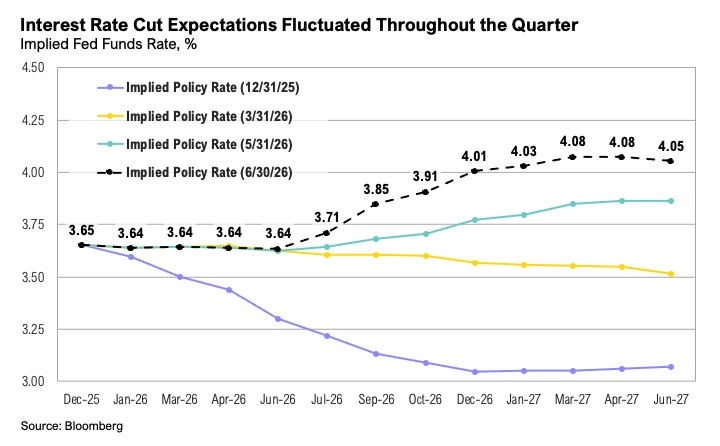

A defining development during the quarter was the beginning of a new Federal Reserve Chair’s tenure (more on this later). As expected, the Federal Reserve left interest rates unchanged throughout the first half of the year.6 However, expectations for the path of rates shifted dramatically as energy prices pushed inflation higher amid the conflict in the Middle East. The rapid repricing reflected two key forces: inflationary pressure stemming from the Iran conflict and the continued resilience of the U.S. economy, underpinned by a resilient labor market and consumer.

Halftime

The U.S.–Iran conflict dominated headlines during the second quarter. Following the outbreak of hostilities on February 28, both countries significantly escalated their military campaigns. The conflict placed the Strait of Hormuz at the center of global attention, disrupting energy flows and contributing to fuel shortages worldwide.7 Tensions peaked in early April, with West Texas Intermediate crude oil rising to $113 per barrel and Brent crude reaching $118.8

Diplomatic efforts gained traction in April when the U.S. and Iran agreed to a Pakistan-mediated ceasefire on April 7, although violations by both sides persisted and the U.S. later imposed a naval blockade on vessels bound for Iranian ports.9 Negotiations remained fragile through May before culminating in a 14-point memorandum of understanding signed on June 17.10 The agreement established a framework for discussions covering navigation through the Strait of Hormuz, Iran’s nuclear and missile programs, and sanctions relief.10 While military operations formally ended, many key issues remain unresolved, and negotiations continue. The 60-day deadline outlined in the June 17 memorandum of understanding expires in mid-August.

Domestic energy markets reflected the impact of the Iran conflict. U.S. crude oil exports reached a record 6.4 million barrels per day in April and remained elevated through mid-June, benefiting domestic producers.11 Even so, gasoline inventories fell to multi-year lows during the quarter, driving a sharp increase in fuel prices. Average pump prices for regular unleaded gasoline rose from $2.80 per gallon in early January to a peak of $4.60 on May 20 before ending June at $3.85.12

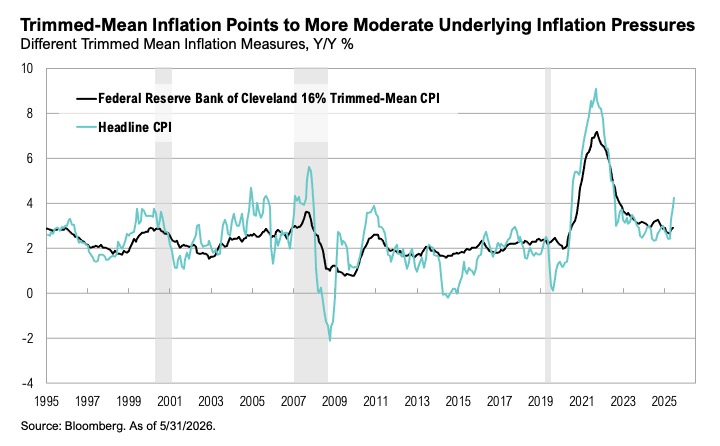

May 15 marked the start of a new era at the Federal Reserve. Kevin Warsh was nominated Federal Reserve Chair in January, and his April confirmation hearing outlined a framework centered on trimmed-mean inflation measures, the removals of forward guidance and the dot plot, and a belief that AI-driven productivity gains will ultimately prove disinflationary.13,14 Those themes remained front and center at his first Federal Open Market Committee meeting on June 16–17. At the post-meeting press conference, Warsh announced five task forces focused on Fed communications, balance sheet policy, data sources, productivity and AI, and the inflation framework.15

The newly established task forces suggest a broad review of how monetary policy is communicated, implemented, and evaluated.15 The most consequential changes may emerge from the inflation framework review. Warsh appears focused on whether traditional headline inflation measures adequately capture underlying price pressures, and he seems interested in placing more emphasis on trimmed-mean measures that exclude extreme price movements.15,16

A shift toward gauges such as the Cleveland Fed Trimmed Mean CPI would place greater emphasis on inflation trends rather than short-term volatility, potentially influencing both policy decisions and how inflation risks are communicated to markets. The Cleveland Fed’s 16% Trimmed-Mean CPI is derived from the Bureau of Labor Statistics’ CPI data and is calculated by excluding the most extreme price increases and decreases each month (approximately the highest 8% and lowest 8% of weighted price changes) and averaging the remainder, providing a clearer measure of underlying inflation trends.17

Despite a mixed political and economic backdrop, the U.S. consumer remained resilient throughout the second quarter and the first half of 2026. Consumer fundamentals remain healthy, and both personal income and spending (at 0.7% month-over-month in May) remained above five-year averages of 0.4% and 0.5%, respectively.18,4 The Johnson Redbook Index (a higher-frequency datapoint which measures the weekly same-store sales at major U.S. retailers) rose to the highest non-pandemic-fueled level on record.19 Evidence emerged during the quarter that lower-income consumers may be recovering. According to PNC Bank credit card data, the spending gap between upper- and lower-income households narrowed from 4.5% at the end of 2025 to approximately 1.5% by June. Cash savings buffers for lower-income households also increased from 25 days to more than 30 days.20 Similarly, Bank of America data showed that lower-income household spending reached its highest level in three years during June.21

Importantly, the 2026 FIFA World Cup was unlikely to be the primary driver of the strength. Most World Cup-related spending occurs in lodging, dining, transportation, and ticketing, categories that are not well captured by the Redbook Index. However, other data sources reflected strong activity. OpenTable (a measure of key restaurant performance metrics, guest spending behavior, and seated diner traffic) reported a 40% year-over-year increase in seated diners during the final week of June.22

Consumers may see relief on certain goods’ prices in the coming months. On February 20, the Supreme Court ruled that President Trump lacked the authority to impose tariffs under the International Emergency Economic Powers Act (IEEPA), effectively invalidating the April 2025 “Liberation Day” tariffs.23 On March 4, 2026, the U.S. Court of International Trade ordered Customs and Border Protection to refund at least $165 billion in improperly collected tariffs, injecting liquidity back into businesses and consumers.24 According to court filings, as of the end of June, $71 billion had effectively been refunded, with $100 billion in the pipeline.25,26 Walmart is expected to receive roughly $2.4 billion.27 As Walmart CFO John Rainey noted:

“We think the single best return that we can have on a dollar of capital right now is to invest in the consumer and invest in price.”28

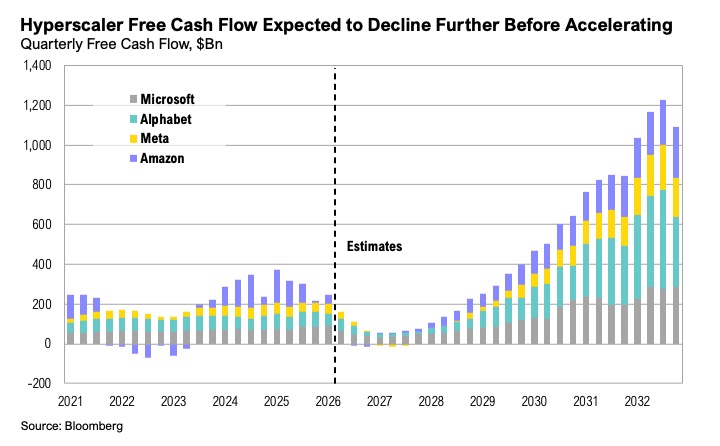

Since the launch of ChatGPT in November 2022, the five largest U.S. hyperscalers (Amazon, Microsoft, Meta, Alphabet, and Oracle) have driven the largest corporate investment cycle on record. Capex increased from $156 billion in 2023 to $443 billion in 2025 and is expected to reach $700 billion in 2026 and over $900 billion in 2027.29 Some estimates suggest that AI-related capex accounted for around 50% of U.S. GDP growth in 2025.30 AI-related spending on data centers, chips, and networking equipment accounted for about 0.8% of U.S. GDP in the first quarter of 2026, helping push total computing infrastructure investment to 1.5% of GDP—more than double its average share between 2015 and 2022.31 Effectively, the AI hyperscalers have been sponsoring much of the strength in the U.S. economy and in equity markets for nearly four years. This trend shifted in the first half of 2026. As AI capex accelerated, free cash flow came under pressure. Alphabet’s first-quarter free cash flow fell 47% year-over-year, while Amazon’s declined 95% under the weight of AI infrastructure spending.29

Market breadth (the percentage of stocks participating in a market advance or decline) improved steadily during the second quarter. More than 60% of S&P 500 constituents ended the period above their 200-day moving averages.32 U.S. small-cap stocks outperformed their large-cap counterparts by 6%, while a broader mix of companies reached new highs. This suggests that market leadership may be expanding beyond the mega-cap technology companies that have dominated returns in recent years. Earnings expectations for the remainder of 2026 support this view. Energy (66%), Information Technology (49%), and Materials (39%) are expected to lead S&P 500 earnings growth, while overall index earnings are projected to increase by 24% on 11% revenue growth.33

Markets

Looking Forward

We are focused on how the AI buildout transitions from a story of capacity expansion to one of monetization, profitability, and broader economic productivity. The key question is whether hyperscalers’ AI spending will generate enough returns to support expectations for more than 20% S&P 500 earnings growth in 2026 and continued margin expansion across industries. Meta’s decision to lease excess AI compute highlights a growing debate around whether bottlenecks are easing and if supply is catching up with demand. Ultimately, the next phase of the AI trade may be defined less by who builds the infrastructure and more by which companies successfully convert AI adoption into sustainable revenue growth, margin expansion, and free cash flow.

We are monitoring the outcomes of Kevin Warsh’s five Federal Reserve task forces, particularly whether they result in changes to how inflation is measured and to Fed communications, including a potential shift toward trimmed-mean inflation measures. Beyond monetary policy, we are watching the reopening of the IPO market, an evolving supply backdrop for U.S. equities, and signs that market leadership is broadening beyond AI capex beneficiaries toward sectors such as Healthcare, Financials, Energy, and Real Estate.

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

Citations

- Bureau of Labor Statistics: https://www.bls.gov/news.release/empsit.nr0.htm

- Challenger, Gray & Christmas: https://www.challengergray.com/blog/challenger-report-june-layoffs-cool-to-45849-down-53-from-may-ai-leads-reasons-for-fourth-consecutive-month/

- Bureau of Economic Analysis: https://www.bea.gov/data/consumer-spending/main

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/CES0500000003#

- IRS: https://www.irs.gov/newsroom/filing-season-statistics-for-week-ending-may-8-2026

- Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/series/FEDFUNDS

- IEA: https://www.iea.org/topics/the-middle-east-and-global-energy-markets

- OilPrice.com: https://oilprice.com/oil-price-charts/

- CNBC: https://www.cnbc.com/2026/04/07/trump-iran-ceasefire-hormuz-strait.html

- Reuters: https://www.reuters.com/world/middle-east/14-point-draft-us-iran-deal-2026-06-17/

- U.S. Energy Information Administration: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WCREXUS2&f=W

- AAA: https://gasprices.aaa.com/

- Wall Street Journal: https://www.wsj.com/economy/central-banking/key-moments-from-kevin-warshs-congressional-testimony-1e1cec0b

- Bloomberg: https://www.bloomberg.com/news/articles/2026-04-21/kevin-warsh-s-fed-confirmation-hearing-key-takeaways-on-interest-rates-policy

- Federal Reserve: https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20260617.pdf

- Wall Street Journal: https://www.wsj.com/economy/central-banking/kevin-warsh-wants-the-fed-to-think-about-inflation-differently-64272e0a

- Federal Reserve Bank of Cleveland: https://www.clevelandfed.org/indicators-and-data/median-cpi

- Bureau of Economic Analysis: https://www.bea.gov/data/income-saving/personal-income

- MacroMicro: https://en.macromicro.me/charts/23462/us-redbook-same-store-index

- PNC: https://www.pnc.com/content/dam/pnc-com/pdf/aboutpnc/EconomicReports/consumer_health_check/PNC_Research_Consumer_Health_Check_June_2026.pdf

- Bank of America: https://institute.bankofamerica.com/content/dam/economic-insights/consumer-checkpoint-july-2026.pdf

- OpenTable: https://www.opentable.com/c/state-of-industry/#seated-diners-chart

- Reuters: https://www.reuters.com/legal/government/us-supreme-court-rejects-trumps-global-tariffs-2026-02-20/

- Reuters: https://www.reuters.com/world/us/judge-orders-trump-administration-finalize-goods-entering-us-without-assessing-2026-03-04/

- Cato Institute: https://www.cato.org/blog/ieepa-refunds-update-good-progress-still-ways-go

- U.S. Court of International Trade: https://storage.courtlistener.com/recap/gov.uscourts.cit.17610/gov.uscourts.cit.17610.39.0.pdf

- CNBC: https://www.cnbc.com/2026/05/22/trump-tariff-refunds-walmart-home-depot-target-apply.html

- NPR: https://www.npr.org/2026/05/21/nx-s1-5829712/walmart-price-cuts-gas-tariff-refunds

- Bloomberg data series

- Bank for International Settlements: https://www.bis.org/publ/bisbull120.pdf

- Epoch AI: https://epoch.ai/data-insights/ai-datacenter-share-gdp

- Bloomberg data series

- FactSet: https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_071026.pdf

Index Definitions

The S&P 500 Index is widely regarded as the best single gauge of the United States equity market. It includes 500 leading companies in leading industries of the U.S. economy. The S&P 500 focuses on the large cap segment of the market and covers approximately 75% of U.S. equities.

The S&P 500 Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight – or 0.2% of the index total at each quarterly rebalance.The S&P 500® Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight – or 0.2% of the index total at each quarterly rebalance.

The Bloomberg Barclays U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Duration is roughly 5 years.

The Bloomberg U.S. Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. It includes approximately 2000 of the smallest US equity securities in the Russell 3000 Index based on a combination of market capitalization and current index membership. The Russell 2000 Index represents approximately 10% of the total market capitalization of the Russell 3000 Index. Because the Russell 2000 serves as a proxy for lower quality, small cap stocks, it provides an appropriate benchmark for RMB Special Situations.

The U.S. Dollar Index is used to measure the value of the dollar against a basket of six foreign currencies: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

MSCI U.S. REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs). The index is based on the MSCI USA Investable Market Index (IMI), its parent index, which captures the large, mid and small cap segments of the USA market. With 150 constituents, it represents about 99% of the US REIT universe and securities are classified under the Equity REITs Industry (under the Real Estate Sector) according to the Global Industry Classification Standard (GICS®), have core real estate exposure (i.e., only selected Specialized REITs are eligible) and carry REIT tax status.

The MSCI China Index captures large and mid cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). The index covers about 85% of this China equity universe. Currently, the index includes Large Cap A and Mid Cap A shares represented at 20% of their free float adjusted market capitalization.

The MSCI India Index is designed to measure the performance of the large and mid cap segments of the Indian market. With 165 constituents, the index covers approximately 85% of the Indian equity universe.

Disclaimers

*Source: MSCI.MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

The opinions and analyses expressed in this newsletter are based on Curi Capital, LLC’s (“Curi Capital”) research and professional experience are expressed as of the date of our mailing of this newsletter. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is it intended to speak to any future time periods. Curi Capital makes no warranty or representation, express or implied, nor does Curi Capital accept any liability, with respect to the information and data set forth herein, and Curi Capital specifically disclaims any duty to update any of the information and data contained in this newsletter. The information and data in this newsletter does not constitute legal, tax, accounting, investment or other professional advice. Returns are presented net of fees. An investment cannot be made directly in an index. The index data assumes reinvestment of all income and does not bear fees, taxes, or transaction costs. The investment strategy and types of securities held by the comparison index may be substantially different from the investment strategy and types of securities held by your account.