The Waypoint: Q3 2022 Market Commentary

Navigators use waypoints to ensure they’re on the correct path. While a flight path may look like a straight line on a map, it’s actually a series of very minor course corrections—and staying the course is critical.

In 1979, a New Zealand airplane with 257 people on board crashed into the side of an Antarctica volcano due to white-out conditions and the use of incorrect coordinates, just 2 degrees off, in the plane’s navigation. Think about that—a mere 2 degrees from target led to complete disaster. [1]

With the summer in full swing and half the year behind us, this is a great time to check your financial plans and investment portfolios to see if any adjustments are needed to stay on course.

HALFWAY CHECKPOINT

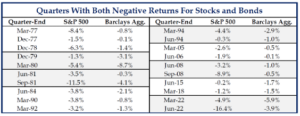

Let’s begin by assessing where we are at the 2022 midpoint. The first six months of 2022 were historically bad for both stocks and bonds. There are only 5 out of 186 quarters since 1976 where both stocks and bonds were negative for two consecutive quarters, and the first half of 2022 was one of them.

Stocks, as measured by the S&P 500 Index, were down -4.9% for Q1 and -16.4% for Q2, putting first half performance at -20.0%. Bonds, which are considered the safety piece of many investor portfolios, were down -5.9% in Q1 and -4.7% in Q2, bringing the Bloomberg US Aggregate Bond Index down -10.4% through June 30. [2]

Source: Strategas Securities, LLC as of June 30, 2022

Past performance doesn’t guarantee future results. It is possible to lose money up to your invested principal.

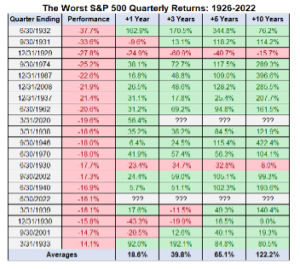

However, history does offer some solace. While no two time periods are exactly alike and past performance is not an indication of future results, stock market declines of this magnitude have usually been followed by positive performance 1, 3, 5, and 10 years out. The major exception to this being the Great Depression, as the table below demonstrates. Spoiler alert: We do not believe we’re in for another Great Depression, or even a Great Recession.

Source: Ben Carlson, A Wealth of Common Sense, July 6, 2022.

Past performance doesn’t guarantee future results. It is possible to lose money up to your invested principal.

THE INFLATION IMPACT

We believe the primary driver of markets and the economy this year is sustained high inflation that turned out to be more than “transitory.” There are still many supply and demand imbalances from the pandemic, and the war in Ukraine and latest Omicron Covid wave have contributed to continued high inflation.

With full employment, the U.S. Federal Reserve must bring inflation down to meet one of its two mandates. As such, the Federal Reserve is aggressively raising rates and ceasing easy monetary policies (Quantitative Easing) in place from the Great Financial Crisis.

Financial conditions are significantly tighter now than they were last year, and the consequences are numerous. Higher interest rates, lower valuations for all financial assets (including stocks), and less liquidity in the system most acutely witnessed in speculative assets—like cryptocurrencies and profitless tech stocks—have become the norm.

RECESSION FEARS

Going forward, we should expect the U.S. Federal Reserve to continue raising rates for the remainder of the year. While many economists are increasingly worried about the dreaded “r word”, recession, we don’t see the Fed easing up on rate hikes until inflation decidedly moves lower—or labor markets deteriorate meaningfully from here. Neither seem likely in the next few months.

While recession fears naturally spook investors, we believe the economic slowdown will be relatively mild. Consumers and corporate America are in strong financial health, and banks are much healthier than they were heading into the Great Financial Crisis, so contagion risk seems lower.

A recession could be a good thing in the long-run as it might resolve the supply-demand imbalances caused by the pandemic. Slower economic growth should help alleviate pricing pressures throughout the economy, including housing, labor markets, autos, and energy and food prices.

INVESTMENT OPPORTUNITIES LIE AHEAD

For investors, it’s important to remember that markets tend to lead the economy. Many believe the significant declines felt in the first half of the year are the market signaling a recession in the not-too-distant future. While we are not calling a market bottom and it will take awhile for the market to repair the damage done, we do think the worst of the pain is behind us.

We also believe that markets are much less expensive today than they were at the beginning of the year. Bond investors have endured years of low yields, and the first six months were a severe adjustment to rising rates; however, yields are much higher now than in the beginning of the year, so new investments and reinvested proceeds from existing bonds will generate significantly more yield than last year.

Equity investors can take comfort in knowing that most of the S&P 500 Index decline is attributable to a lower price-to-earnings valuation and not lower earnings providing some cushion to an expected earnings decline in coming months.

As long-term investors, our team at Curi Capital is extremely excited about the investment opportunities that we believe lie ahead. We are focusing our time and effort searching for promising investment opportunities to deliver to our clients.

If you are interested in reviewing your portfolio, discussing potential actions, or exploring what Curi Capital can do for you, please reach out to a member of the Curi Capital team at 984-202-2800.

Please note: This material should not be considered a recommendation to buy or sell securities or a guarantee of future results. Curi Capital is a registered investment advisor. Registration does not imply a certain level of skill or training. More information about Curi Capital can be found in its Form ADV Part 2, which is available upon request.

Past performance is not a guarantee of future results. All investment strategies have the potential for profit or loss; changes in investment strategies, contributions, or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

[1] https://www.bbc.com/news/world-asia-50555046

[2] Grabinski, Ryan and Bohnsack, Nicholas, Strategas Securities, LLC “Daily Macro Brief,” July 1, 2022

READ NEXT

Meet the Curi Capital Team: Spotlight on Hannah Arthur, Senior Client Service Administrator

At Curi RMB Capital, it’s our mission to help clients build true wealth, however they define it. Our team brings the knowledge, experience, and passion aiming to help clients meet their goals through a wide range of financial services and solutions—and we’d love for you to meet them. Get to know Hannah Arthur, Senior Client Service Administrator

Nurturing Generosity: Teaching Philanthropic Values Across Generations

Senior Wealth Manager, Sheldon Fox, shares insights into how philanthropic values and a culture of giving can be shared across generations.

Happy New Year!: Q1 2024 Market Commentary

Mark Paccione provides several timely action items you can take to best prepare your investment portfolio for what’s to come in the year ahead.